1.1 Executive Summary

On 17 March 2026, the SEC published a joint interpretive release with the CFTC that classifies crypto assets into five categories.1 The central conclusion: most crypto assets are not securities. Only “digital securities,” meaning traditional financial instruments represented as tokens, remain subject to the full US securities law framework. For European issuers and platforms, the interpretation invites direct comparison with two EU frameworks: MiCA (which regulates crypto-assets that are not financial instruments) and MiFID II (which regulates those that are). Swiss issuers face an additional layer of analysis under the Swiss financial market regulations. The classification logic converges on tokenized securities. It diverges on disclosure obligations and on the lifecycle of a security classification.

You will learn:

- How the SEC’s five-category taxonomy compares to the EU’s classification framework under MiCA and MiFID II

- Why tokenized securities are the area of least regulatory friction between the US, the EU, and Switzerland

- Where the MiCA whitepaper obligation may create tension with the SEC’s investment contract analysis, and how reverse solicitation fits in

- How the SEC’s classification lifecycle mechanism differs from the EU’s static approach

- What European issuers and platforms should do now

1.2 The SEC’s Five-Category Taxonomy

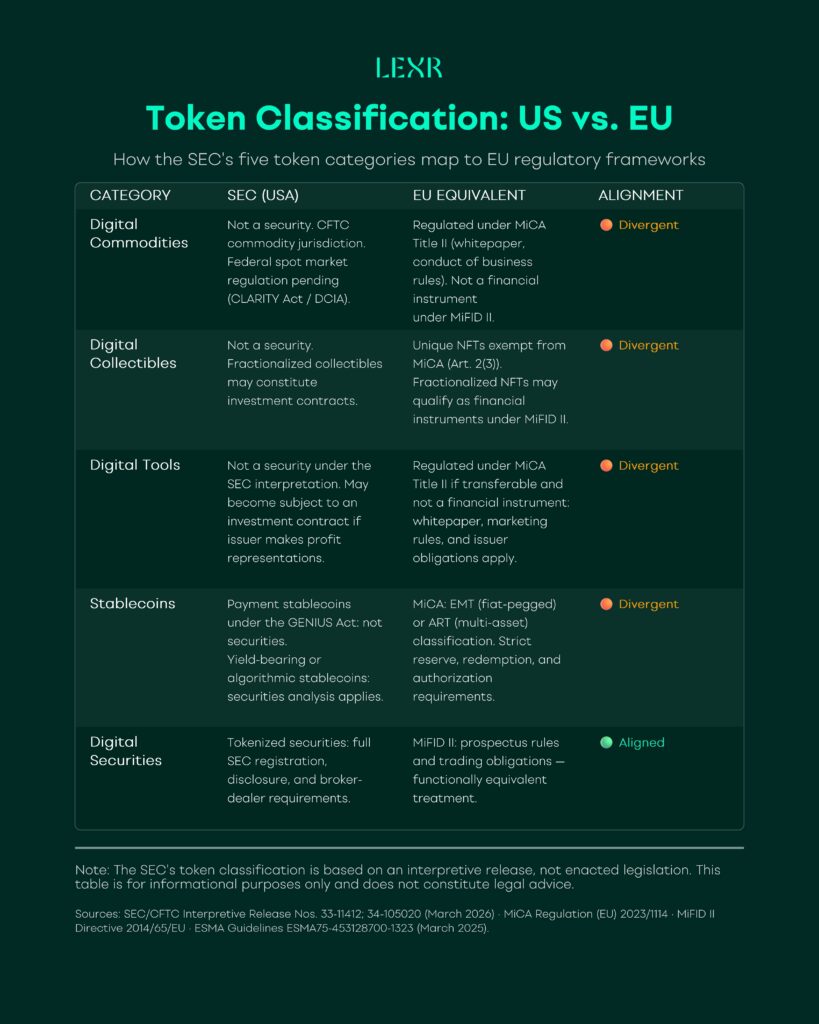

The SEC interpretation establishes a token taxonomy that covers the entire crypto asset universe. Five categories, four of which are explicitly not securities.2

Digital Commodities are crypto assets that are intrinsically linked to and derive their value from the programmatic operation of a functional crypto system, as well as supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others. The interpretation names a sample list of 16 assets, including BTC, ETH, SOL, XRP, ADA, AVAX, LINK, DOT, XLM, HBAR, LTC, DOGE, SHIB, XTZ, BCH, and APT.3 Not securities.

Digital Collectibles are crypto assets designed to be collected or used, representing rights to artwork, music, videos, trading cards, in-game items, or digital representations of internet memes and cultural references. Not securities.

Digital Tools are crypto assets that perform a practical function, such as a membership, ticket, credential, title instrument, or identity badge. Not securities.

Stablecoins as defined in the GENIUS Act, meaning payment stablecoins issued by a permitted payment stablecoin issuer. Not securities. This category is narrower than it appears at first glance: it covers only payment stablecoins under the GENIUS Act. Yield-bearing or algorithmic stablecoins that do not meet this definition may still be subject to securities analysis.4

Digital Securities (or “tokenized securities“) are financial instruments enumerated in the definition of “security” that are formatted as or represented by a crypto asset, where the record of ownership is maintained in whole or in part on or through one or more crypto networks. Securities.

The interpretation also addresses the boundary between these categories. Under US law, a token that is not itself a security can still be sold as part of an investment contract – essentially, an arrangement where someone invests money based on the issuer’s promises to build or manage something that will generate returns. If the issuer later fulfils those promises or clearly fails to deliver, the investment contract ends, and the token is no longer subject to securities law. The SEC further clarified that protocol mining, protocol staking, wrapping of non-security crypto assets, and certain airdrops do not involve the offer and sale of a security.5

Two points of context are important. First, the document is a joint interpretive release (Release No. 33-11412), not a formal rule adopted through notice-and-comment rulemaking. It supersedes prior SEC staff statements on topics including meme coins, stablecoins, mining, and staking.6 Second, Chairman Atkins has announced that the SEC plans to launch a formal rulemaking process within weeks, with proposals reportedly expected to exceed 400 pages and to include a detailed “innovation exemption” for crypto firms.7 European issuers with US market ambitions should closely monitor that process.

1.3 Classification Logic: How SEC Howey Analysis Compares to ESMA’s MiFID II Guidelines and Swiss Regulations

Both the SEC and ESMA approach the classification question from the same starting premise: the legal treatment of a token depends on its economic substance, not its technical format. The two frameworks differ in legal tradition but reach comparable outcomes for the category that matters most.

The SEC applies a reworked version of the Howey test. A crypto asset becomes subject to securities law when it is offered as part of an investment contract, meaning an investment of money in a common enterprise with an expectation of profits derived from the essential managerial efforts of others.8 The four non-security categories are carved out because, by their characteristics, they do not meet this test.

ESMA’s March 2025 guidelines apply a three-criteria test under Article 4(1)(44) of MiFID II.9 A crypto asset qualifies as a transferable security when it is not a payment instrument, belongs to a class of securities with standardised rights, and is negotiable on capital markets. Technology plays no role in the assessment.

Under Swiss laws, a security is a right which is standardised and suitable for mass trading; irrespective of its form. According to current Swiss practice, FINMA generally rejects classifying both payment and utility tokens as securities. The reason for this is that payment tokens are intended as a means of payment and so they do not present any similarities to traditional securities based on their economic function. Likewise, utility tokens are not analogous to securities because they are not connected to the capital market. By contrast, FINMA considers asset tokens to be securities if they represent an uncertificated security and are standardised and suitable for mass trading.

The convergence point is tokenized securities. A tokenized bond, a tokenized share, or a tokenized fund unit, irrespective of whether issued on a blockchain natively or whether in form of a wrapped traditional security, qualifies as a security under all three frameworks. Neither system treats the blockchain as a distinguishing factor.

Where the approaches diverge is in scope. The SEC taxonomy covers the entire crypto asset universe in a single document and explicitly carves out non-securities categories. ESMA’s MiFID II guidelines address only the boundary between financial instruments and MiCA-regulated crypto-assets. The EU does not have a single taxonomy covering all token types in a single document. Instead, the classification is split across MiFID II (for financial instruments), MiCA (for crypto-assets that are not financial instruments), and the Prospectus Regulation (for disclosure obligations). Similarly, Switzerland does not rely on a single comprehensive taxonomy, but instead applies a principles-based, case-by-case classification under FINMA guidance.

1.4 Tokenized Securities: The Area of Least Friction

The SEC defines digital securities as financial instruments that are “formatted as or represented by a crypto asset, where the record of ownership is maintained in whole or in part on or through one or more crypto networks.”10 Under MiFID II, tokenized financial instruments are defined through Article 4(1)(15), which was amended to explicitly include instruments “issued by means of distributed ledger technology.”11

The practical result is that a tokenized bond issued in the EU under MiFID II and a tokenized bond recognised as a digital security under the SEC interpretation are subject to equivalent regulatory treatment in their respective jurisdictions. Prospectus or registration requirements apply. Investor classification rules apply. Trading venue and custody regulations apply.

In Switzerland, FINMA treats tokenized securities under the same financial market laws that apply to their traditional equivalents, consistent with its technology-neutral approach. For Swiss issuers looking at both the US and EU markets, the structural alignment across all three jurisdictions on tokenized securities is notable: a tokenized bond is a security in Zurich, Frankfurt, and New York. The operational differences (which disclosure document, which investor categories, which venue authorisation) are significant but manageable. The regulatory conflict sits elsewhere.

1.5 The Disclosure Tension: MiCA Whitepapers and US Investment Contract Risk

This is where the two systems may create tension for issuers, and where European founders need to pay close attention.

MiCA requires a whitepaper before any public offering of a crypto-asset that falls within its scope.12 The whitepaper must include a description of the project, the rights and obligations associated with the token, the underlying technology, associated risks, information on governance, the use of funds raised, and sustainability disclosures. It must be submitted to the national competent authority at least 20 working days before publication. The issuer is legally liable for inaccurate or misleading content. Since 23 December 2025, the whitepaper must be published in machine-readable iXBRL format using the ESMA MiCA taxonomy.13

The SEC interpretation takes a different approach to issuer communications. A non-security crypto asset may become subject to an investment contract when the issuer “offers it by inducing an investment of money in a common enterprise with representations or promises to undertake essential managerial efforts from which a purchaser would reasonably expect to derive profits.”14 The interpretation specifies that several factors increase the risk: the source of the communication (issuer versus third party), the timing (pre-launch versus post-functional network), the channel (official communications versus community discussion), and the level of detail (specific milestones, timelines, personnel, and funding allocation).

The conflict is structural. A MiCA-compliant whitepaper may contain, by regulatory requirement, exactly the type of detailed forward-looking information that the SEC framework identifies as a potential investment contract trigger. Project timelines, funding allocation, development milestones, team descriptions: all mandatory under MiCA, all risk factors under the SEC interpretation.

For a token that is a non-security under the SEC taxonomy but requires a MiCA whitepaper in the EU (utility tokens, governance tokens, certain access tokens), the issuer faces a real problem. Publishing the whitepaper fulfils EU obligations but may create US securities law exposure if the document is accessible to US investors. This tension does not apply to tokenized securities, which are already classified as securities in both jurisdictions and subject to structurally parallel disclosure obligations.

The tension sits in the middle category: tokens that both systems recognise as non-securities by nature, but where the EU mandates transparency, and the US penalizes the type of transparency that MiCA requires.

Reverse solicitation does not resolve this. European issuers sometimes point to MiCA’s reverse solicitation provisions (Article 61) as a mechanism to limit US exposure. In our reading, this is a misapplication of the concept. Reverse solicitation governs whether a third-country firm may serve EU clients without MiCA authorisation when the client initiates contact. It does not address, and cannot solve, the question of whether a publicly accessible MiCA whitepaper creates US investment contract exposure. Geographic restrictions on document access (such as IP blocking or US-targeted disclaimers) may reduce but do not eliminate this risk. Issuers in this position need jurisdiction-specific communication strategies, not a single document designed to satisfy both regimes simultaneously.

1.6 Custodian and Staking Obligations: A Practical Divergence for Platforms

The SEC interpretation includes specific guidance on staking that European platforms should not overlook. Protocol staking, where a user directly stakes non-security crypto assets and receives protocol-generated rewards, does not involve the offer and sale of a security. However, the interpretation explicitly excludes three custodial arrangements from this safe treatment: custodians that guarantee staking yields (because guaranteed returns imply discretionary managerial efforts), custodians that unilaterally decide when, whether, or how much of a client’s assets to stake, and custodians that lend, pledge, or rehypothecate deposited assets.15

For EU-based CASPs (crypto-asset service providers) that are MiCA-licensed and also serve US clients or hold US-originated assets, these exclusions create a compliance obligation that goes beyond MiCA’s own custody and staking rules. A CASP that offers “staking-as-a-service” with guaranteed yields may comply with MiCA but simultaneously trigger US securities law obligations. This is a different type of cross-border friction than the whitepaper issue, but it follows the same structural logic: conduct that is permitted and regulated in one jurisdiction may be unregulated or differently regulated in the other.

1.7 The Classification Lifecycle: A Conceptual Gap Between US, Swiss, and EU Law

The SEC interpretation introduced a mechanism with no direct EU equivalent. A non-security crypto asset can become subject to an investment contract and can subsequently cease to be subject to one. The investment contract terminates when the issuer has fulfilled its representations or has failed to satisfy them.16

Under EU law, the classification of a financial instrument under MiFID II does not have a comparable exit mechanism. A transferable security remains a transferable security. The legal status is determined by the characteristics of the instrument, not by the issuer’s ongoing conduct. Under MiCA, a crypto-asset that is not a financial instrument may change its classification if its characteristics change (for example, if a utility token acquires financial instrument features). But MiCA or MiFID II do not provide a mechanism by which a regulated crypto-asset ceases to be regulated because the issuer completed a project.

This difference reflects a broader divergence in regulatory philosophy. The SEC framework, rooted in the Howey test, focuses on the transaction and the relationship between issuer and investor. When that relationship changes, the regulatory status can change. The EU framework focuses on the instrument and its characteristics. The regulatory status follows the instrument’s features, not the issuer’s conduct. Swiss law sits between the two approaches. FINMA applies a principle-based assessment, but qualification as a security requires a contractual claim between issuer and token holder. This made the treatment of pre-functional utility tokens particularly relevant: FINMA’s position is that such tokens qualify as securities until the underlying infrastructure is sufficiently complete. Once it is, the token holder no longer holds claims against the issuer — and the security classification falls away. The logic is structurally similar to the SEC’s completed-representations mechanism, though the Swiss model is less formalised — there is no explicit lifecycle provision, and the underlying concept differs: Swiss law focuses on the existence of a contractual claim, while the SEC framework focuses on the issuer’s representations and the investor’s reasonable expectation of profit.

For issuers, the practical implication is straightforward. In the US as well as in Switzerland, there may be a path out of securities regulation for certain tokens once the project matures and the issuer’s representations have been fulfilled. In the EU, the classification is more stable and less dependent on issuer behaviour. European issuers should not assume that a US “exit” from securities status translates into any change in their EU regulatory obligations.

1.8 A Note on Permanence

The SEC interpretation is a joint interpretive release, not legislation. Chairman Atkins has noted that only Congressional action can make the framework permanent. The CLARITY Act (Digital Asset Market Clarity Act of 2025, H.R. 3633) passed the House in July 2025 with a 294-134 vote. The Senate Agriculture Committee advanced a related bill, the Digital Commodity Intermediaries Act (S. 3755), in January 2026. The Senate Banking Committee has not yet completed its markup, and several key issues (including stablecoin yield provisions and DeFi oversight) remain unresolved.17 Prediction markets currently price the probability of a presidential signature in 2026 at approximately 72%. Until that legislation is enacted, the interpretation can be changed by a future SEC chair. European issuers should factor this into their compliance planning: the current framework is directionally clear but not yet legally durable.

1.9 Key Takeaways for European Issuers and Platforms

Tokenized securities are the area of convergence. A tokenized bond is a security in the US, the EU, and Switzerland. Issuers should plan for parallel compliance, with jurisdiction-specific execution on disclosure, investor classification, and venue access.

MiCA whitepaper content may create US exposure risk for non-security tokens. The forward-looking statements that MiCA requires are the same statements that the SEC identifies as investment contract triggers. Review whitepaper content for US risk before publication. Reverse solicitation does not solve this problem. Consider jurisdiction-specific communication strategies.

Staking and custody arrangements need cross-border review. MiCA-licensed CASPs that guarantee staking yields or exercise discretion over client assets may trigger US securities obligations. Align your staking product design with both frameworks before launch.

The classification lifecycle works differently. The US, in certain aspects similar to Switzerland’s treatment of pre-functional tokens, offers a potential exit from securities status when issuer representations are fulfilled. The EU does not. Do not assume that a US classification change affects EU obligations.

The SEC framework is not yet permanent. The CLARITY Act would codify the taxonomy. The Senate process is ongoing, with a realistic but not guaranteed path to enactment before the November 2026 midterms. Monitor the formal rulemaking (including the innovation exemption) that Atkins has announced for the coming weeks.

Map all applicable frameworks before making decisions. Communication strategies, token structuring, and platform listing decisions should account for the SEC taxonomy, MiCA, MiFID II, and (for Swiss-based issuers) the DLT Act. The convergences simplify compliance for tokenized securities. The divergences on disclosure, staking, and classification lifecycle require jurisdiction-specific planning for everything else.

Next Steps:

Do you need clarity on how the SEC taxonomy interacts with your MiCA or Swiss regulatory obligations? LEXR advises European issuers and crypto platforms on cross-border regulatory strategy, including MiCA compliance, US securities law exposure, and jurisdiction-specific communication strategies. Contact us to discuss your project.

Footnotes:

- SEC and CFTC, Interpretation on the Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets, Release No. 33-11412, 17 March 2026. ↩︎

- SEC Fact Sheet, Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets (17 March 2026). ↩︎

- The interpretation names 16 crypto assets as examples of digital commodities: Bitcoin (BTC), Ether (ETH), Solana (SOL), XRP, Cardano (ADA), Avalanche (AVAX), Chainlink (LINK), Polkadot (DOT), Stellar (XLM), Hedera (HBAR), Litecoin (LTC), Dogecoin (DOGE), Shiba Inu (SHIB), Tezos (XTZ), Bitcoin Cash (BCH), and Aptos (APT). Algorand (ALGO) and LBRY Credits (LBC) are named separately in the release as additional examples. The interpretation presents these as examples, not an exhaustive list. ↩︎

- The GENIUS Act (Pub. L. 119-27) defines “permitted payment stablecoin issuer” and the conditions under which payment stablecoins are excluded from the securities framework. Yield-bearing stablecoins or stablecoins structured as investment products are not covered by this exclusion. ↩︎

- Release No. 33-11412, Sections V (Protocol Mining and Protocol Staking), VI (Wrapping), and VII (Airdrops); SEC Fact Sheet at p. 3. ↩︎

- It expressly supersedes the SEC staff’s 2019 Framework for “Investment Contract” Analysis of Digital Assets. As a Commission-level interpretation, it also effectively displaces prior staff-level statements on meme coins, stablecoins, mining, and staking, though these are not individually named as superseded in the release. ↩︎

- Remarks by Chairman Atkins at the DC Blockchain Summit, 17 March 2026 (as reported by CoinDesk, Blockhead, and others). ↩︎

- SEC v. W.J. Howey Co., 328 U.S. 293 (1946), as applied in Release No. 33-11412. ↩︎

- ESMA, Guidelines on the conditions and criteria for the qualification of crypto-assets as financial instruments (ESMA75-453128700-1323), Final Report 17 December 2024, published 19 March 2025. ↩︎

- Release No. 33-11412, Section II(E) (Digital Securities). ↩︎

- Directive 2014/65/EU (MiFID II), Article 4(1)(15), as amended by the DLT Pilot Regime Regulation (EU) 2022/858. ↩︎

- Regulation (EU) 2023/1114 (MiCA), Title II, Article 4. ↩︎

- Commission Implementing Regulation (EU) 2024/2984 (forms, formats, and templates for crypto-asset white papers). The iXBRL format requirement applies since 23 December 2025. ESMA published the MiCA XBRL taxonomy on 5 August 2025. ↩︎

- Release No. 33-11412, Section III (Investment Contract Analysis); SEC Fact Sheet at p. 2. ↩︎

- Release No. 33-11412, Section V.B (Protocol Staking). ↩︎

- Release No. 33-11412, Section III(C) (Termination of Investment Contract Status); SEC Fact Sheet at p. 2. ↩︎

- CLARITY Act (Digital Asset Market Clarity Act of 2025), H.R. 3633, 119th Congress. Passed the House on 17 July 2025 (294-134). Senate Agriculture Committee advanced the Digital Commodity Intermediaries Act (S. 3755) on 29 January 2026. Senate Banking Committee markup pending as of March 2026. Key unresolved issues include stablecoin yield provisions, DeFi oversight, and the Trump administration’s conflicts-of-interest provisions. ↩︎